The growth and success of farmer producer organisations (FPOs) is determined by a crucial element: their financing.

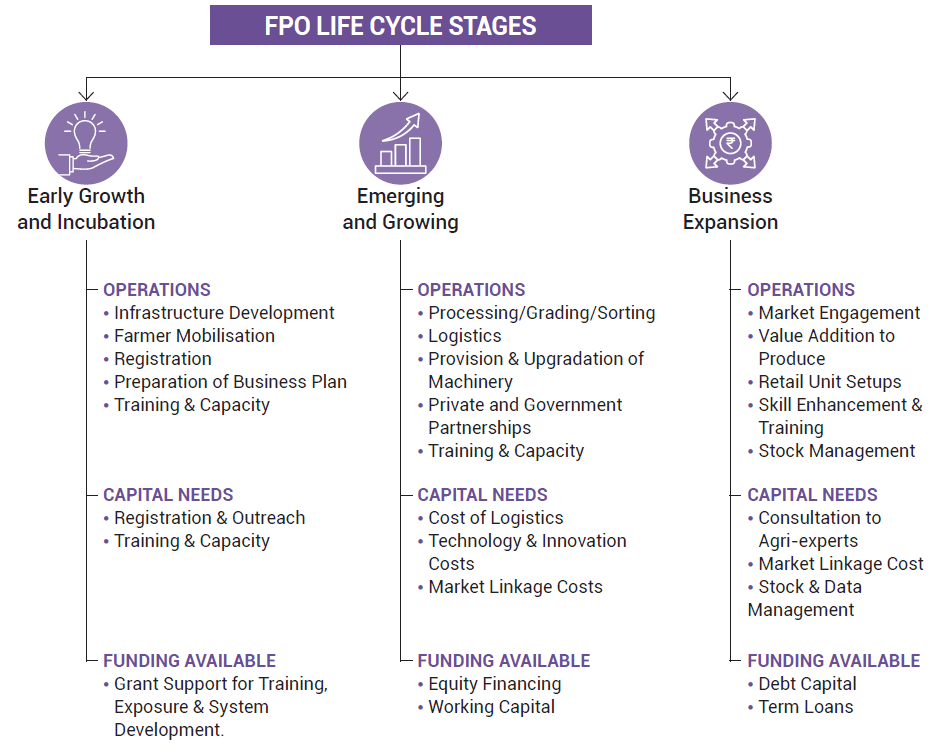

Financing requirements for FPOs vary by the activities across the life cycle, from pre-incubation to incubation, and consolidation stages. As FPOs progress through their life cycle, their financing requirements evolve to support different activities and objectives. Understanding the diverse financial needs and challenges faced by FPOs at each stage is essential for designing effective financing strategies and enabling their full potential.

Grant support is crucial during the pre-incubation stage to establish operations and mobilise farmers. Government agencies and promoting organisations, such as the National Bank for Agriculture and Rural Development (NABARD) through its Producer Organisation Development Fund (PODF), have been instrumental in providing grant and incubation support to FPOs in their early years. Furthermore, several donors including the World Bank, Ford Foundation, Rabo Foundation, and others have played a vital role in supporting capacity development and strengthening the governance of FPOs.