While India’s credit market has been expanding since the pandemic, it is the least robust among its Asian peers, due to bottlenecks within its financial data sharing systems.

Affordable and accessible credit is instrumental to economic growth. Account Aggregators (AA) are enabling this by simplifying data sharing systems for Indian borrowers.

Conceptualised by the Reserve Bank of India, account aggregators are entities that collect and provide access to financial information of a customer, based on their consent, to financial information users (FIUs). The RBI developed the framework and guidelines for account aggregators as a part of its regulatory initiatives to promote digital innovation and enhance financial services in the country.

The Building Blocks of AA

The Data Protection and Empowerment Architecture (DEPA), developed by the RBI, provides the underlying infrastructure and principles for data sharing. It forms the final layer of India Stack – a series of digital public goods designed to improve digital services for India across a range of sectors.

Technology standards

Enabling regulations

Network participants

Account Aggregators utilise the DEPA architecture, and act as the technology and service layer that facilitates the actual implementation of data aggregation and sharing.

Account Aggregators

Marketplace

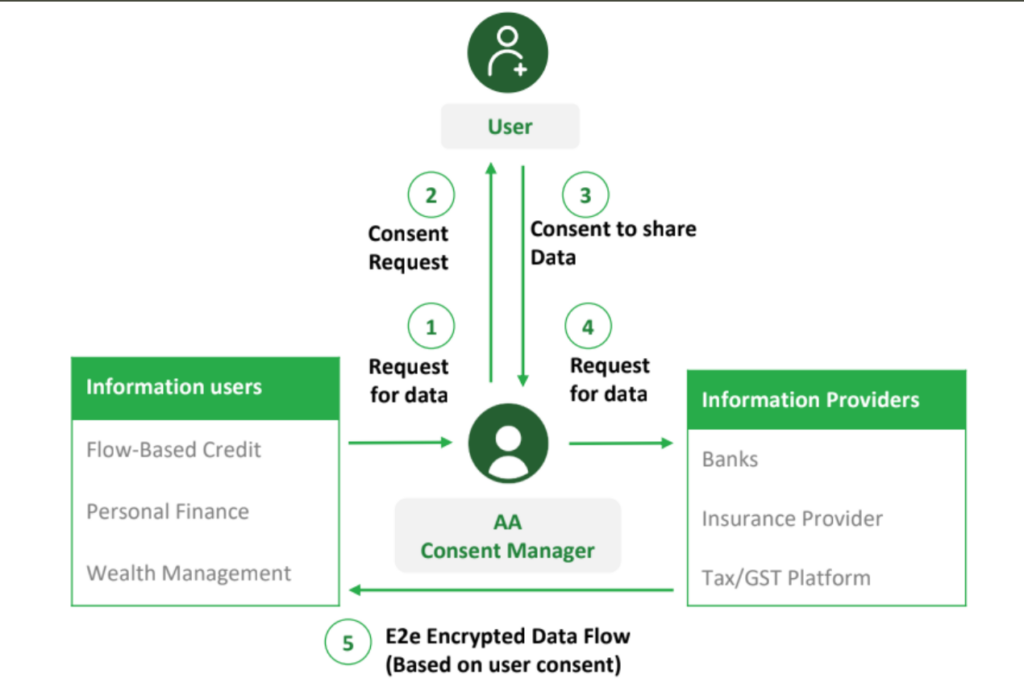

The Mechanics of AA

How does this mechanism address existing issues?

Account Aggregators

- enable the consolidation of data stored across multiple institutional databases.

- eliminate the need for cumbersome data-gathering processes by providing a secure platform for individuals to connect their accounts without physical visits or sharing confidential information.

- establish standardised processes and protocols for porting data across institutions, simplifying and streamlining the transfer of data.

- ensure robust security measures for individuals, mitigating data misuse.

- Users provide explicit consent to the AA for collecting their data, which is then gathered from multiple sources, and organised for easy analysis and presentation.

- Users can securely access aggregated financial data through a user-friendly dashboard. They have granular control over data-sharing permissions and can manage access as desired.

- Data requests from FIUs consist of specific requirements and user consent.

- The AA validates user consent and retrieves authorised financial data, while ensuring authenticity, security

and privacy. This is then delivered to the FIU, for for customer insights, credit assessment, and personalised services.

- Individual users possess complete control over their data, and consent can be set to expire. They can also choose to share their data with only specific institutions.

- AAs help FIUs save time and resources, by eliminating manual data collection, while providing a holistic view of customers’ financial information. The comprehensiveness of data allows for a thorough assessment of creditworthiness and financial health, allowing FIUs to serve customers more effectively with personalised solutions.

What impedes the adoption of Account Aggregators?

Addressing the design and implementation challenges to AAs can help them realise their full potential in catalysing financial inclusion.

- One of the primary design challenges for AAs is creating awareness and adoption of the ecosystem among potential users. As the AA ecosystem is still in its early stages, many users may not be aware of its benefits, leading to slow adoption rates.

- Data privacy and security are crucial design challenges for the AA ecosystem. The ecosystem collects and stores sensitive customer financial data, and it is essential to

ensure that this data is protected from unauthorised access or misuse. - The technical complexity of the AA ecosystem can also be a design challenge, as it requires the integrating various systems and technologies. Ensuring interoperability among different systems and platforms can be a significant challenge.

- The implementation costs of the AA ecosystem can be high, as it requires significant investments in technology, infrastructure, and compliance.

- The regulatory framework for the AA ecosystem is still evolving, which can create implementation challenges for AA providers. As the regulatory framework is still being developed, AA providers may face challenges complying with regulations and guidelines.

- Another implementation challenge for the AA ecosystem is the limited participation of financial institutions. To be effective, the ecosystem needs the participation of a large number of financial institutions. However, many financial institutions may hesitate to

participate due to regulatory and technical challenges.