On this page

Overview

The Digital Platforms team under Sattva Knowledge Institute, in partnership with Sahamati, launched Communities of Practice (CoP), which focused on the role of Account Aggregators in simplifying micro-credit for nano-enterprises in India. The session gathered a cohort of leaders and practitioners spanning various sectors, all sharing a common focus on accelerating financial inclusion through our emerging Digital Public Infrastructure (DPI).

The three primary objectives of the CoP were:

- Deliberating on systemic issues that hinder digital financial inclusion for nano-enterprises

- Understanding Account Aggregators (AA) with use cases

- Co-create public goods that improve the deployment of AAs to meet the micro-credit needs of nano-enterprises

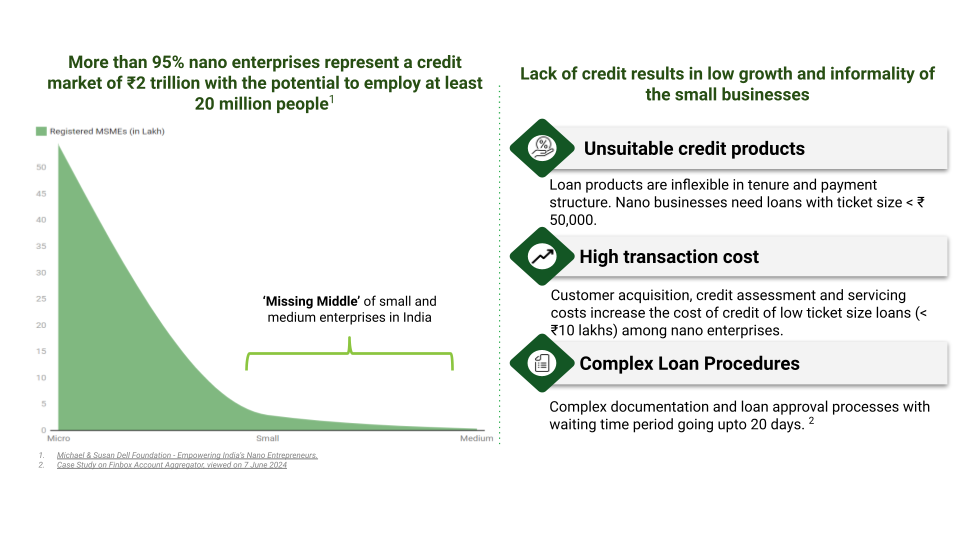

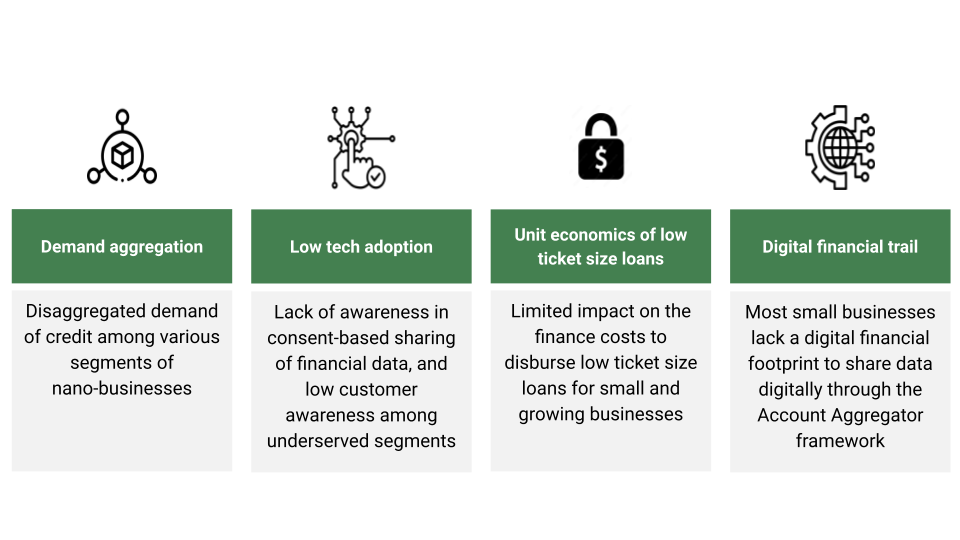

We identified four key challenges that obstruct credit to micro- and nano-entrepreneurs:

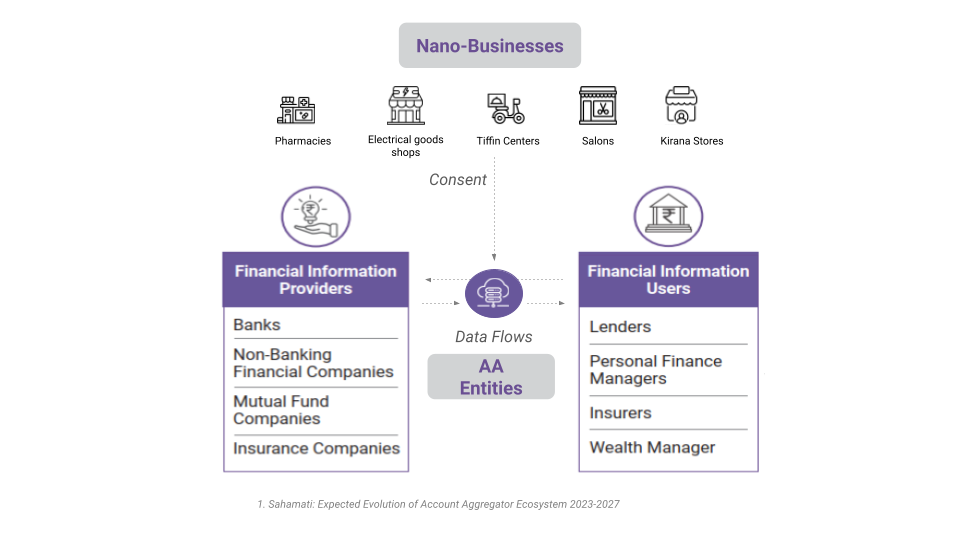

Account Aggregators can create a digital financial identity and empower millions of MSMEs through digital access and financial data sharing across institutions.

Solution Hypotheses

A clear distinction between nano-enterprises and other categories is essential for developing a more inclusive lending framework. The CoP emphasised the need for a clear definition with established quantitative criteria for identifying nano-businesses. The group proposed a multi-criteria approach that considers different turnover revenue in shops based on the region and type of business.

- The discussion acknowledged the diverse risk-reward profiles within this segment, advocating for a broader definition that encompasses gig workers and commission-based service professionals

- The delineation should incorporate factors like investment in working capital and the daily operational needs of the business.

- Existing thresholds, such as the ₹40 lakh turnover limit for GST registration and the ₹3 lakh annual income limit in microfinance, can be considered as potential reference points.

The discussion identified a critical challenge – assessing the creditworthiness of unregistered nano-enterprises. Assessing the creditworthiness of unregistered nano-enterprises through traditional methods is challenging due to several factors. These enterprises typically lack formal financial documentation such as bank statements, income tax returns, and GST filings. Small businesses often operate on a cash basis without proper bookkeeping and have no established credit history. Additionally, regulatory constraints mean these businesses fall outside the formal financial system, making it difficult to evaluate their financial stability using conventional metrics. There is a need for alternative approaches for comprehensive credit assessment of small businesses.

- Business growth potential, type of business, and the entrepreneur’s capabilities are crucial aspects of risk assessment.

- Credible data sets that serve as proxy data to assess businesses such as utility bill payments, analysis of bank transaction data, and information from third-party platforms collecting data relevant to the lender’s risk assessment.

- Analysing bank account activity, such as the percentage of funds retained, frequency of UPI transactions, and overall level of activity can be enabled by real-time consumption data accessible through APIs.

However, informed and explicit consent from borrowers to share financial data is necessary for any approach utilising such data.

Customised credit score card for nano-business based on credible data sources

Leveraging alternate data sources can provide a more holistic understanding of the borrower’s profile to reflect a customised credit score.

- The credit scorecard is based on app data combined with personal, business, and financial information, so lenders can gain a more comprehensive view of the business.

- This framework would involve assigning different weights to various data points, creating a combined financial score that reflects not just credit history, but also transaction patterns, account balances, payment behaviour, and overall level of formal financial activity. Account aggregators can facilitate the secure transfer of this data.

- This, in turn, allows lenders to build credit scoring models based on the shared data and underwrite borrowers more comprehensively.

However, this approach requires educating borrowers about improving their scores. Incentivising them to adopt digital and formal business practices can significantly contribute to this goal.

Loan collection is a big challenge in the nano-business category. Extensive geographic coverage for loan recovery demands a large investment in resources, which increases overall loan costs. Currently, loan costs to lenders range from 22-35% per annum, with operational expenses (opex) and loan collection costs consuming a substantial portion (3-5%). This necessitates robust collection strategies to improve the predictability of loan recoveries and reduce the burden of collections.

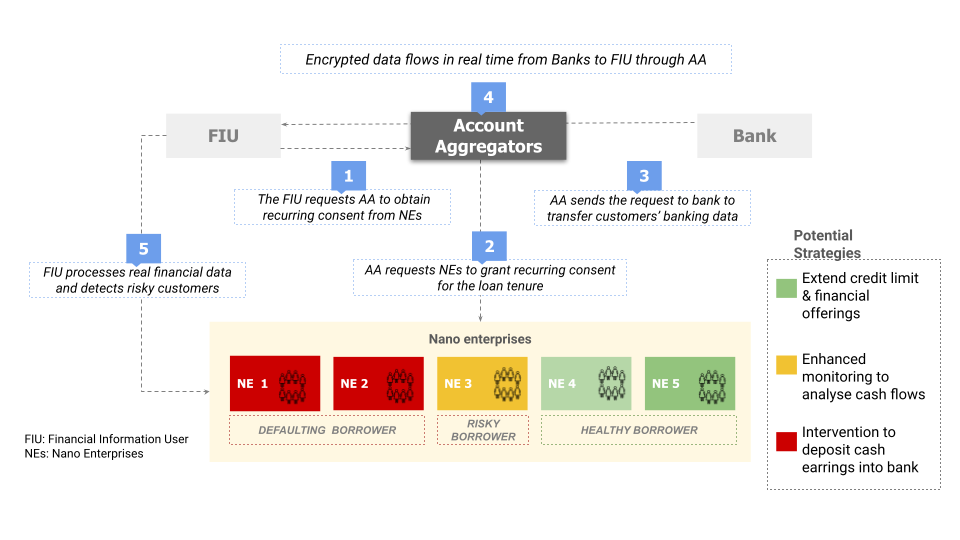

Real-time data extracted through Account Aggregators (AAs) offers a solution by triggering early warning signals for potential defaulters, enabling timely interventions.

Key Steps:

- Recurring Consent: During loan disbursal, the Financial Institution (FIU) obtains recurring consent from the borrower for the loan period.

- Data Acquisition: The AA requests access to the borrower’s bank accounts and other available financial data points.

- Nano-business Consent: The nano-business grants recurring consent for sharing bank account statements throughout the loan tenure.

- Data Collection: The AA’s public infrastructure facilitates the acquisition of relevant data, including account receivables (bank statements) and new sales and purchase data.

- Financial Health Analysis: The FIU utilises recurring bank statements to assess the borrower’s financial health.

- Early Warning System: Based on the analysis, the FIU determines loan collectability and sets up early warning systems to identify potentially risky customers.

- Targeted Intervention: The FIU proactively intervenes with nano-businesses exhibiting potential repayment challenges.

The data is categorised into three segments based on transaction activity:

- Healthy Borrowers (Green): These borrowers exhibit regular transactions and healthy revenue streams, indicating their ability to make timely EMI payments. The frequency of transactions is ideally 20-30 per month, providing the bank with a clear picture of their income.

- Sporadic Transactions (Yellow): These borrowers have inconsistent banking activity and revenue inflow. FIUs can analyse their monthly cash flows to assess their repayment capacity.

- Defaulters (Red): These borrowers lack any banking transactions since the loan disbursement, offering limited visibility into their repayment potential. For this segment, lenders can utilise their resources for targeted interventions, potentially incentivising them to deposit earnings into a bank account and reassess their repayment capacity.

Leveraging real-time data and early intervention strategies makes loan collection more predictable. This allows lenders to focus resources on high-risk borrowers rather than expending significant effort on geographically dispersed, low-risk clients.

Over 9,000 RBI-regulated NBFCs and MFIs could participate in the Account Aggregator (AA) framework. Presently, only a small fraction (2 MFIs, 3 SFBs, and 185 NBFCs) use it actively. Increasing adoption among Financial Institutions (FIUs) is crucial to unlock the potential of AA for nano-business lending. However, a key barrier for smaller NBFCs and MFIs is the high up-front effort required for integration and maintenance within the AA framework. These institutions, which are best positioned to serve small businesses, face multiple challenges:

- High upfront technology costs and ongoing maintenance fees.

- Lack of a standardised digital onboarding experience for users, creating an unfamiliar user interface that hinders last-mile adoption.

- Limited technical expertise to provide a seamless digital experience for borrowers.

To address these challenges and enable low-cost FIU integration with AA, while simultaneously improving the borrower’s digital experience, a reference app can be built as a digital public good specifically catering to organisations lending to underserved segments. This open-source, white-label app would serve two key purposes:

- Improve User Experience: Built on the digital needs of the last-mile user, it will offer features like voice-enabled assistance and integration with regional languages (Bhashini-enabled) to enhance user experience for small businesses.

- Low- cost Tech Integration: FIUs can either use the app directly, or integrate its APIs with their existing digital products, significantly reducing the cost and complexity of integration with the AA framework.

The reference app will be built on five core principles:

- Open-source white-label app: Freely available for FIUs to deliver digital financial services.

- User-centric design: Inspired by best practices for small businesses, including features like voice assistance and regional language support.

- Digital onboarding for non-digital entities: Enables institutions like microfinance institutions (MFIs) and Regional Rural Banks (RRBs) to transition their paper-based loan application processes to a digital platform.

- Credit-focused journey: Starts with core credit functionalities like working capital and short-term loans, with the ability to expand to other financial services in the future.

- Reduced development costs: Lowers the barrier to entry for socially-focused lenders by providing a pre-built foundation for innovation in the sector.

To ensure successful implementation, several considerations are important:

- Assisted journeys: Since many borrowers may require assistance, explicit consent for data sharing needs to be obtained after clearly explaining all terms and conditions.

- Data privacy compliance: The reference app must adhere to all Digital Personal Data Protection (DPDP) guidelines set forth by the Indian government.

- Regulatory sandbox testing: The solution should be rigorously tested within the RBI’s regulatory sandbox environment before being deployed for lending institutions.

A reference app can play a vital role in driving financial inclusion for nano-enterprises by addressing these challenges and considerations.

Nano enterprises are scattered in different pockets of various regions. These geographically dispersed businesses often rely on informal lending to meet their operational credit needs. Discovering and servicing these businesses is difficult due to the high customer acquisition cost, which constitutes 3-5% of the overall credit cost. There is a need for a cost-effective model that aggregates micro-credit demand. This challenge could be addressed through the use of a Demand Signalling Platform which could be a valuable tool to aggregate pockets of micro-credit to unlock credit for these non-online nano-enterprises.

In order to fulfil this logistically, over 500 community-based organisations (CBOs) already work directly with small entrepreneurs. These CBOs can play a crucial role as credit enablement partners by aggregating a large number of nano-enterprises. They can ensure demand aggregation, assess credit behaviour, and support both credit delivery and repayment. By leveraging authentic sources, CBOs can aggregate business data, and signal credit demand to lenders willing to service these businesses. A demand signalling platform can facilitate this process, enabling CBOs to aggregate the credit demand of nano-enterprises, and allowing registered lenders to discover and cater to these demands easily.

Way Forward

At the Sattva Knowledge Institute, our primary focus is on a crucial element of social impact – developing infrastructure-enabling solutions. Our goal is to establish foundational infrastructures and public goods that empower innovators to make a greater impact. Moving forward, we will strengthen Communities of Practice to highlight the relevance of solution-enabling infrastructure in accelerating formal financial inclusion in India through the following work:

- Market research on understanding the digital & tech capabilities of Non-Banking Financial Institutions (NBFCs) & Microfinance Institutions (MFIs) to deliver digital financial services to underserved segments

- Testing Technology pathways to build a community reference app built on the experiential needs of the last-mile user

- Engage the philanthropic ecosystem to build strong evidence on the low unit economics of microcredit lending through DPIs

We will build new research based on the inputs from the session & identify opportunities for collaborative action.

Refer to our previous work here: